Quick Definition: Self employment income is the revenue you earn from running your own business, freelancing, or contracting, minus the expenses you incur to earn it. Unlike a salary, self employment income is not fixed, is not subject to automatic withholding, and is reported differently to the CRA. The amount you actually keep depends on your gross earnings, your deductible business expenses, and your tax and CPP obligations, all of which you manage yourself.

Introduction

When you move from a salaried job to self-employment, the income side of your life changes in ways that go well beyond just how much you earn. The structure of income itself is different. A salary is simple: a fixed amount arrives in your bank account on a regular schedule, already stripped of taxes and deductions. Self employment income is more complicated, more variable, and potentially more valuable, but only if you understand how it actually works.

Most people switching to self-employment underestimate how different these two income types are. They compare their old salary to their new freelance rate as if they are equivalent, and then they are surprised at tax time when the numbers do not add up the way they expected. Understanding self employment income before you start earning it, or before your first tax return arrives, saves real money and real stress.

This article covers how self employment income is defined, how it is calculated, how it is taxed, how it is reported to the CRA, and what the practical differences are between earning a salary and running your own income.

What Is the Difference Between Self Employment Income and a Salary?

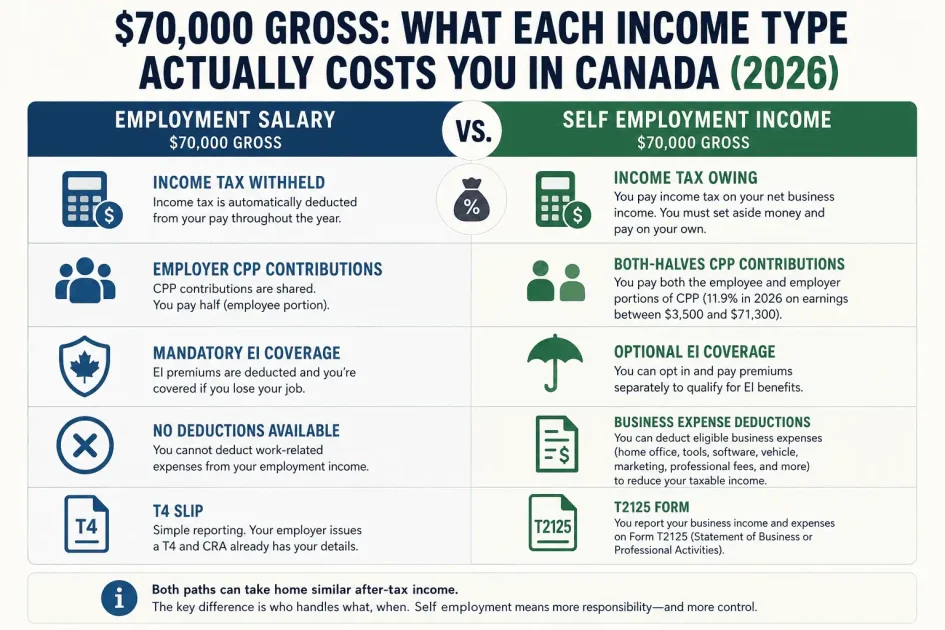

A salary is compensation paid by an employer under a contract of service. It is fixed, predictable, and processed through payroll. Before you see a dollar of it, your employer has already calculated and remitted income tax, CPP contributions, and EI premiums to the CRA on your behalf. Your T4 slip at year-end documents exactly what you earned and what was withheld.

Self employment income is revenue earned under a contract for services, typically from multiple clients, where you are responsible for the work, the business risk, and all of your own tax obligations. Nobody withholds anything. The gross amount your client pays hits your account, and from that point forward, setting aside money for taxes, calculating CPP contributions, and managing GST/HST is entirely your responsibility.

The practical difference is significant. A salaried employee earning $70,000 knows exactly what their take-home pay will be each month. A self-employed person earning $70,000 in gross revenue might take home considerably more or considerably less, depending on their business expenses, their CPP contributions, their province, and how well they managed their tax obligations throughout the year.

How Self Employment Income Is Calculated

This is where most people get tripped up, and it is worth being precise.

Gross self employment income is the total revenue you received from clients before any deductions. If you invoiced $80,000 in a calendar year, your gross self employment income is $80,000.

Net self employment income is what remains after you deduct eligible business expenses from your gross income. If you had $15,000 in legitimate business expenses (home office, equipment, software, professional development, vehicle use for business), your net self employment income is $65,000.

This distinction matters enormously because the CRA taxes your net self employment income, not your gross. CPP contributions are also calculated on net self employment income. The higher your legitimate business deductions, the lower your net income, and the lower your tax and CPP bill. This is the main financial advantage of self employment over salary: employees generally cannot deduct work-related expenses, while self-employed Canadians can deduct a wide range of costs that directly reduce their taxable income.

The formula is straightforward:

Gross revenue minus eligible business expenses equals net self employment income

Net self employment income is then added to any other income you earned in the year, and the total is subject to federal and provincial income tax at your marginal rate.

How a Salary Is Taxed vs How Self Employment Income Is Taxed

This is the comparison most people need to understand clearly before making the switch from employment to self-employment.

Salary taxation

When you earn a salary:

- Your employer calculates income tax based on your salary and withholds it from each paycheque

- Your employer deducts your share of CPP contributions (5.95% in 2026 on earnings between $3,500 and $71,300) and matches that amount from their own budget

- Your employer deducts EI premiums (1.66% on earnings up to $68,900 in 2026) and pays a matching 1.4 times that amount on your behalf

- At year-end you receive a T4 slip showing what you earned and what was deducted

- Your tax return is typically straightforward: enter your T4 numbers, claim standard credits, and either receive a refund or pay a small balance

Self employment income taxation

When you earn self employment income:

- Nobody withholds anything; your gross invoice amount arrives in your account

- You are responsible for income tax on your net self employment income (federal plus provincial)

- You pay both the employee and employer halves of CPP: a combined 11.9% on net earnings between $3,500 and $71,300 in 2026, up to a maximum contribution of $8,460.90

- There is also CPP2: an additional 8% on net earnings between $71,300 and $81,200

- EI is optional; you can opt in to access special benefits (illness, parental, caregiving) for a premium of $1.63 per $100 of earnings up to $68,900, capped at $1,123.07 for 2026; regular EI for job loss is not available

- You must register for GST/HST and remit it to the CRA once your revenue exceeds $30,000 in four consecutive calendar quarters (GST/HST collected is not income, but it does pass through your account)

- You report self employment income using Form T2125 (Statement of Business or Professional Activities) as part of your T1 personal return

- Your filing deadline is June 15, but any balance owing is due April 30; missing the April 30 payment triggers daily compound interest regardless of the later filing date

- If you expect to owe more than $3,000 in tax, the CRA will expect quarterly instalments, not just a lump sum at year-end

The CPP difference alone is one of the most significant financial adjustments. An employee on a $70,000 salary pays approximately $3,960 in CPP. A self-employed person with $70,000 in net income pays approximately $7,920, because they cover both halves. That $3,960 difference was previously paid by the employer. Now it comes directly from the self-employed person’s pocket.

Business Expense Deductions: The Key Advantage of Self Employment Income

The main financial offset for the higher CPP burden and the administrative complexity of self employment income is the ability to deduct legitimate business expenses from gross revenue before calculating tax.

Employees cannot deduct most work-related costs. If you are a salaried employee and you buy a new laptop for work, that cost comes out of your after-tax income. If you are self-employed and you buy a new laptop for your business, that cost reduces your taxable income before tax is calculated.

The CRA requires that business expenses be incurred for the purpose of earning business income and be reasonable in the circumstances. Common deductible expenses for self-employed Canadians include:

Home office: If you work from home and use a dedicated space exclusively for business, you can deduct a proportional share of household expenses including rent or mortgage interest, utilities, internet, and home insurance. The deduction is calculated based on the percentage of your home’s total area used for business.

Vehicle use: If you use a personal vehicle for business purposes (client visits, job sites, business errands), the business-use percentage of fuel, insurance, maintenance, and depreciation is deductible. A mileage logbook is essential, as the CRA frequently audits vehicle deductions.

Equipment and technology: Computers, cameras, phones, tools, and other equipment used to earn business income. Large purchases may need to be depreciated over several years (capital cost allowance) rather than deducted fully in the year of purchase.

Software and subscriptions: Business-related software, cloud subscriptions, and professional tools are fully deductible in the year paid.

Professional development: Courses, books, certifications, and training directly related to your business are deductible.

Professional services: Accounting fees, legal fees, bookkeeping, and other professional services related to your business.

Marketing and advertising: Website costs, advertising spend, business cards, and promotional expenses.

Insurance: Business liability insurance and professional indemnity insurance premiums.

Not deductible: personal expenses even if partially related to work, meals and entertainment above the 50% allowed amount, life insurance premiums (with limited exceptions), and personal travel that includes business components unless the primary purpose is business.

The value of deductions compounds at higher income levels. A $15,000 deduction for a self-employed person in a 40% combined marginal tax bracket saves $6,000 in tax. That same $15,000 spent by a salaried employee comes out of after-tax income with no recovery.

T4 vs T4A vs T2125: How Self Employment Income Is Reported

The paperwork differences between salary and self employment income are concrete and worth understanding.

T4 slip: If you are an employee, your employer issues a T4 slip by the end of February showing your employment income, tax withheld, CPP contributions, and EI premiums. You enter these numbers on your T1 return. The T4 is comprehensive and does most of the work for you.

T4A slip: Some clients issue T4A slips (Statement of Pension, Retirement, Annuity, and Other Income) to self-employed contractors showing amounts paid. Not all clients issue T4A slips, and receiving one does not change your reporting obligations. You must report all self employment income whether or not a T4A was issued.

Form T2125: This is the primary form for self-employed Canadians. It is filed as part of your T1 personal return and covers your gross revenue, all allowable business expenses, and your net business income or loss. Line 13500 of your T1 (or 13700 for professional income) captures the net self employment income figure from T2125 and adds it to your total income for the year.

The T2125 is not complicated, but it requires organized records throughout the year. All revenue and all expenses need to be documented with invoices and receipts. This is why separating business and personal banking from the very beginning is strongly recommended: it makes the T2125 preparation straightforward rather than a reconstruction project every spring.

Gross vs Net: Why the Distinction Matters for Income Comparisons

One of the most common errors people make when evaluating self employment income is comparing gross freelance revenue to net salary as if they are equivalent.

They are not.

If you earn $90,000 as a salaried employee, your take-home pay after income tax, CPP, and EI might be approximately $65,000 to $68,000 depending on your province and personal credits.

If you earn $90,000 in gross self employment revenue, the comparison is not straightforward. You first subtract business expenses to arrive at net self employment income. Then you pay income tax on that net amount plus CPP on both halves. But you also deducted those expenses, which reduced your taxable income. And you have no EI premiums unless you opted in.

A self-employed person with $90,000 in gross revenue and $20,000 in legitimate business expenses has net self employment income of $70,000. Their tax and CPP obligations are calculated on that $70,000, not the $90,000. Their effective take-home is a different calculation than a salary-earner’s, and in many cases it is more favourable once deductions are accounted for.

The comparison that matters is not salary vs gross freelance revenue. It is after-tax, after-CPP salary vs after-tax, after-CPP, after-deduction self employment net income. Running that comparison accurately requires knowing your actual business expenses and your provincial tax rate.

Income Variability: The Most Practical Difference

Beyond the tax mechanics, the most day-to-day difference between self employment income and a salary is variability. A salary is fixed by design. Self employment income varies based on how much work you did, how much you charged, and whether clients paid on time.

This variability has two dimensions. The first is month-to-month variation: some months are full, others are quiet. The second is the gap between invoicing and payment: work done in October may not be paid until December or January, which means your cash flow does not match your earnings in the way a salary does.

Managing self employment income variability requires habits that salaried employees rarely develop: maintaining a cash reserve, tracking receivables actively, setting payment terms that encourage prompt payment, and budgeting based on average income rather than expecting every month to look the same.

The upside of variability is that there is no ceiling. A salary is capped by what your employer agrees to pay. Self employment income is capped only by what you can deliver and what the market will bear. For practitioners who develop their skills, build strong client relationships, and price appropriately, self employment income over a three-to-five year horizon often exceeds what comparable employment would have paid.

Early FAQ: Quick Answers

What is the difference between self employment income and a salary?

A salary is fixed compensation paid by an employer through payroll, with income tax, CPP, and EI deducted before it reaches you. Self employment income is revenue from your own business or freelance work, before expenses. Nobody withholds anything from self employment income: you are responsible for income tax, both halves of CPP (11.9% combined in 2026), optional EI premiums, and GST/HST remittance once revenue exceeds $30,000.

How is self employment income calculated in Canada?

Gross self employment income (total client revenue) minus eligible business expenses equals net self employment income. Net self employment income is what the CRA taxes and what CPP contributions are calculated on. Reporting is done through Form T2125 as part of your T1 personal tax return.

Is self employment income taxed more than a salary?

Not necessarily more, but differently. The CPP obligation is higher because you pay both halves. But business expense deductions, which employees cannot access, can significantly reduce your taxable net income. Whether the effective tax burden is higher or lower depends on your income level, your province, and your deduction profile.

Frequently Asked Questions

What counts as self employment income in Canada?

Self employment income includes revenue from freelancing, consulting, contracting, running a sole proprietorship or partnership, and operating a business. It covers professional income, commission income from self-employment, and income from trades. It does not include employment income from a T4 (salary, wages), investment income, rental income, or pension income, which are reported on separate lines of the T1 return.

How do I report self employment income to the CRA?

Self employment income is reported on Form T2125 (Statement of Business or Professional Activities), which is filed as part of your T1 General personal tax return. You enter your gross revenue, deduct eligible business expenses, and arrive at your net business income or loss. This net amount flows to Line 13500 of your T1 (business income) or Line 13700 (professional income) and is added to your total income for the year. If you are also registered for GST/HST, you file a separate GST/HST return.

Do I need to report self employment income if it is small?

Yes. All self employment income must be reported regardless of the amount. There is no minimum threshold below which self employment income is exempt from reporting. The $30,000 threshold applies only to GST/HST registration, not to income reporting. Failure to report income can result in a penalty of 10% of the unreported amount after the first omission.

What is the self employment income tax rate in Canada?

Self employment income is taxed at the same marginal rate as employment income. Canada uses a graduated federal rate structure: 15% on the first $57,375, 20.5% on income from $57,375 to $114,750, 26% from $114,750 to $158,519, 29% from $158,519 to $220,000, and 33% above $220,000 for 2026. Provincial rates apply on top of federal rates and vary by province. Ontario’s combined top marginal rate sits around 53.53% for the highest earners. Most self-employed Canadians in the middle income range face combined marginal rates of 40 to 46%.

Can I have both a salary and self employment income?

Yes, and this is common. If you work a salaried job and also operate a freelance or consulting practice, both income types are reported on the same T1 return. Your employment income appears via your T4. Your self employment income is reported on T2125. Both are added together to determine your total income and tax bracket for the year. CPP contributions apply to both, so if you are already at or near the CPP maximum through your employment, your self employment CPP obligation may be reduced.

How much of my self employment income should I set aside for taxes?

A commonly recommended starting point is 25 to 30% of gross self employment income for most Canadian provinces and income levels. In higher income brackets or provinces with higher provincial rates, 30 to 35% is more appropriate. This estimate should cover income tax and the CPP obligation. Running your numbers through an accountant in your first year and adjusting the percentage from there is the most accurate approach. For a deeper breakdown, see the self-employment tax guide.

What happens if I do not pay self employment income tax on time?

If your tax balance owing exceeds $3,000, the CRA expects quarterly instalment payments rather than a lump sum at year-end. Missing instalment payments triggers interest charges on the overdue amount. The final balance is due April 30 regardless of the June 15 filing deadline for self-employed Canadians. Filing late triggers a penalty of 5% of the balance owing plus 1% per month for up to 12 months. Repeated late filing increases these penalties.

Conclusion: Understanding Your Income Is Part of Running a Business

Self employment income is not just a different source of money. It is a different system, with different mechanics, different tax obligations, and different planning requirements. The people who handle it well are not necessarily earning more than those who struggle with it. They just understand the structure earlier.

The key differences are worth repeating. Self employment income is gross until you subtract expenses; salary is net by the time it arrives. Self employment income carries the full CPP burden; salary splits it with an employer. Self employment income offers deductions that salary does not; those deductions directly reduce your taxable income. And self employment income varies in ways a salary does not, which requires different financial habits to manage well.

None of this is beyond the capacity of someone who is willing to spend a few hours learning how it works. The people who get into trouble with self employment income are usually the ones who assumed it worked like a salary and were surprised when it did not.

For the practical side of managing these obligations, the guide to self-employment challenges covers how to build the habits that make the income management side of self-employment sustainable. And for anyone still weighing up the income comparison between the two paths, the full breakdown in the self employment vs employment guide covers both the financial and lifestyle dimensions.